Retail sales can be either a coincident or lagging indicator, meaning that it either reflects what is going on at the present time or what has recently occurred. For Rhode Island, the most timely data on retail sales is that for retail sales subject to the sales tax. Based on when these taxes are paid and recorded here versus when the sales actually took place, retail sales for Rhode Island is a lagging indicator. Also, retail sales is a very cyclically sensitive indicator, which means the value of retail sales is very sensitive to the overall level of economic activity. The technical term for this is that retail sales are pro-cyclical, since they move in the same direction as the economy.

Like any economic indicator, it too has its limitations: since this is based on retail sales tax collections in Rhode Island, it excludes any items that are not currently subject to taxation, most notably clothing. And there can be distortions. For example, given the very mild winter, winter clothing expenditure very likely fell since the same time last year. If that decline was sufficient to move total retail sales lower than they were last year, the understatement from excluding clothing sales from our sales tax data might not be as large as it typically is. Similarly, since the meals tax in Rhode Island has been 14.7% higher than the regular sales tax rate for several years now, this has distorted "retail sales" for meals over this period -- tending to overstate the overall total. While this may sound like minutia, it is important to understand that every economic indicator has its share of "baggage." I have believed for quite some time now that the indicator any person likes best is probably the one that person knows the least about.

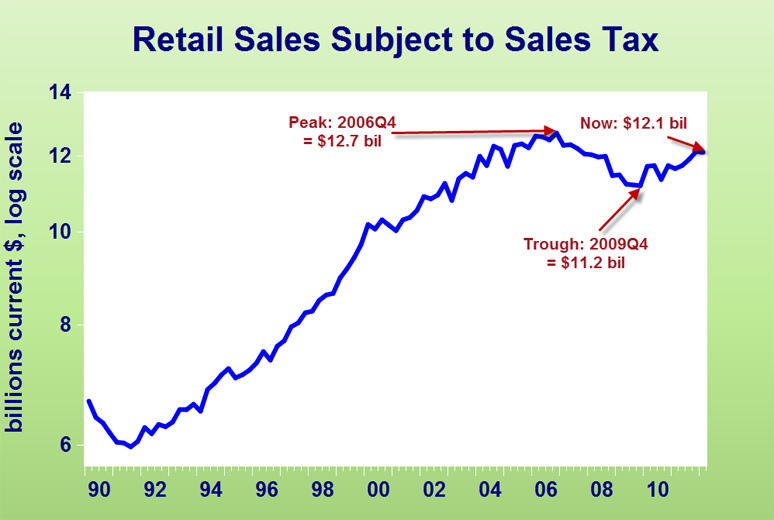

Let's take a look at the historical performance of retail sales in Rhode Island, using as our basis quarterly data on retail sales subject to the sales tax expressed at an annual rate. The chart below (click to enlarge) shows values since the first quarter of 1990. Please note that the vertical axis is stated in logarithms, mainly because a given vertical distance represents the same percentage (relative) change between any two period in the chart.

The most recent peak in retail sales occurred in the fourth quarter of 2006, at $12.7 billion. Can you think of anything else that happened that quarter (hint: we have discussed this numerous times in prior posts)? The answer: it coincides with Rhode Island's most recent employment peak. This reflects the fact that retail sales are very sensitive to the overall level of economic activity, as stated earlier. The trough for retail sales was in the fourth quarter of 2009, at $11.2 billion. Thus, Rhode Island's peak-to-trough decline in retail sales was 11.8 percent. Note that retail sales have trended upward throughout this recovery, although not straight up. Once again, the cyclical nature of retail sales is in evidence here.

This chart provides an excellent illustration of the mindset of most, if not all, of Rhode Island's leaders, its media, and its residents: things here have now turned around nicely, and Rhode Island is doing much better it has in a very long time. Add to this the fact that income tax revenue is up, at least above expectations, and if you read my last post, employment is apparently higher and our state's jobless rate is lower than the currently published data indicate. Thus everything appears to have returned to normal.

I agree totally with the assessment that everything here has returned to normal -- but Rhode Island's "new normal." In economics, we never look at things in absolutes. Instead, we always evaluate things in relative terms. This precludes our making substantive judgments about the behavior of indicators that are stated in current dollars, as retail sales is above. So, let's now turn to evaluating retail sales here in relative terms -- meaning relative to the purchasing power of the present time. This, recall, means examining the historical behavior of real retail sales.

The next chart shows the behavior of real retail sales subject to the sales tax for Rhode Island since 1990 (click to enlarge). As should become readily apparent almost immediately, this gives a very different picture of our current situation.

When taking inflation and purchasing power into account, the peak in real retail sales occurred in the third quarter of 2004, at $14.8 billion. This peak thus came well before the current dollar peak (in 2006Q4). Note that by stating retail sales in the purchasing power of Q1 in 2012, we are "inflating" current dollar values from earlier periods into what they would be if dollars then had the same purchasing power as today, which explains why earlier current dollar values are higher when stated in real terms. The trough in real retail sales occurred in the fourth quarter of 2009, at $11.9 billion. This is the same quarter as the trough in current dollar retail sales.

The reality of Rhode Island's current situation, our "new normal," to quote the phrase coined by Mohammed El-Erian of PIMCO, is in fact very different from the predominant view of our state's economic performance. First, real retail sales here have been falling since the third quarter of 2004, well before our most recent employment peak. Second, the peak-to-trough decline in real retail sales here was much greater than one would conclude based on current dollar values, just under 20 percent. Third, while real retail sales have improved since their trough in 2009Q4, they have registered almost no gain since that time: $12.1 billion versus $11.9 billion. Finally, the most recent trend in real retail sales is sideways to downward. Thus, Rhode Island's economy has failed to perform well enough to consistently generate retail sales growth rates in excess of inflation for quite some time now.

Where does all of this leave us? Not where almost everyone in this state appears to believe. Retail sales data, when viewed in the correct context of real values, confirms something I have written about in more posts than I care to think about, that Rhode Island is in a very tepid recovery. So, even when (or if) current dollar retail sales here exceeds it recent high of $12.1 billion, we will not have returned to anywhere even remotely close to where we once were. So, do we continue to contrast the current situation with the depths of where we once were, as seems to be the dominant view, or should we shift our focus to where we are relative to recent heights? You can guess which I will continue to opt for.

We should be attempting to move toward recent highs -- that should be the standard of excellence or satisfactory performance here. And, guess what? That outcome doesn't just fall on us from heaven. We have to work for it. And very often, this will require that we work very hard to get there. I heard a great saying a few months ago that pertains to this: "Success is not a destination, it is a journey." It's time for Rhode Island to purchase its ticket for this journey, because the dominant perspective here, to dust off an old phrase I used to use to describe Rhode Island about a decade ago, defines success in terms of "Relative Mediocrity."